Digital payments have evolved faster in the last decade than in the previous several decades combined. Consumers now expect payments to be done in the blink of an eye. Moreover, whether it’s an e-commerce purchase, a subscription service, or a peer-to-peer transfer, digital transactions have become the default way of exchanging money.

However, for every successful payment processing, there is a complex system in the backroom. And this is known as payment infrastructure.

In this article, we’ll break down what payment infrastructure actually is, the key components that power it, and how money moves step by step during a digital transaction. By the end, you’ll have a clear understanding of what happens behind the scenes every time you click “Pay Now.”

What Is Payment Infrastructure?

It is the behind-the-scenes system that makes the digital payments work. Even though it feels instant to the businesses and customers, different technologies and financial systems are processing and securing the transaction.

Without it? Businesses would not be able to accept card payments, digital wallets would not function, and services like subscriptions or one-click checkout would not exist. Additionally, payment infrastructure ensures that transactions are not only completed but also verified, secure, and compliant with financial regulations.

Where Payment Infrastructure Is Used?

This system powers almost every kind of modern payment:

➡ E-commerce: Online stores use payment infrastructure to accept card payments, digital wallet payments, and BNPL options at checkout.

➡ Subscription-based businesses: Streaming apps, SaaS companies, and membership services use it for recurring payments, renewals, and automatic billing.

➡ Retail stores: Physical shops use POS systems for card swipes, tap-to-pay, and chip transactions.

➡ Mobile apps: Apps like ride-sharing, food delivery, and fintech platforms rely on it for in-app payments and quick payouts.

➡ Marketplaces: Online marketplaces use it to split payments among buyers, sellers, and platform fees, ensuring everything is settled securely.

Key Components of Payment Infrastructure

Digital transactions don't happen through a single system. Several key components work together to make them possible.

1. Payment Gateway

The payment process starts with a payment gateway. You can also consider it as a digital checkout counter. It collects a customer’s payment details during checkout and securely encrypts the information before sending it ahead for processing.

2. Payment Processor

The payment processor takes the payment information from the gateway and sends it to the right systems for verification. Further, it helps make sure the payment is approved or declined correctly.

3. Acquiring Bank

Also called the merchant’s bank, the acquiring bank receives the payment on behalf of the business. After the approval, it ensures that the funds are transferred to the merchant’s account.

4. Issuing Bank

It is the bank that issued the customer’s credit or debit card. This bank usually checks whether the customer has enough funds or credit. Next, it approves or declines the transaction based on that.

5. Payment Networks

When any transaction is made, payment networks act as a bridge for all the parties involved. In the U.S., the most common ones include Visa, Mastercard, American Express, and Discover. For payment infrastructure, they set the rules and help route transactions between issuing and acquiring banks.

6. Fraud Prevention & Security Systems

Around 71% of businesses faced payment fraud attacks in 2023. Because of this, strong security and authentication have become key parts of a reliable payment infrastructure. These systems make sure every payment is safe and legitimate. They protect both customers and businesses using tools like:

➡ Tokenization: Hides card details by replacing them with a secure token.

➡ Encryption: Protects payment information while it is being transferred.

➡ 3D Secure: Adds an extra verification step to confirm the payment is genuine.

➡ Risk Monitoring: Looks for suspicious transactions and helps prevent fraud.

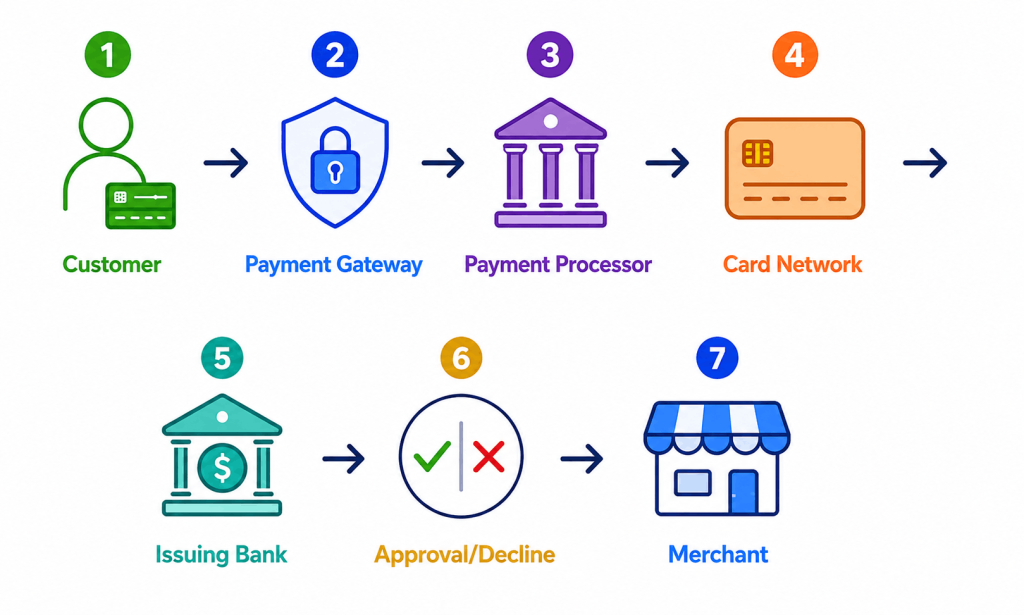

How Payment Infrastructure Works?

Here’s the step-by-step guide on how the enterprise payment infrastructure system works.

Step 1: Customer Initiates Payment

At first, the customer chooses a payment method and clicks “Pay.” This could be a credit card, debit card, digital wallet (like Apple Pay or Google Pay), bank transfer, or BNPL option.

Step 2: Payment Gateway Collects Data

The payment gateway securely collects the customer’s payment details at checkout. It encrypts the information, so sensitive data is protected before it moves further in the system.

Step 3: Payment Processor Routes the Request

Next, the payment processor takes the encrypted data and sends it through the payment network. It makes sure that the request reaches the right banks.

Step 4: Issuing Bank Authorizes the Transaction

The issuing bank checks the transaction. Later, it verifies things like available balance or credit limit and runs fraud checks to ensure the payment is legitimate.

Step 5: Approval or Decline

The issuing bank either approves or declines the transaction, and it is based on the verification. This response is sent back to the merchant in just a few seconds.

Step 6: Settlement and Fund Transfer

If approved, the transaction moves to the settlement stage through the payment infrastructure. Depending on the payment method, this step can happen in different ways. In some cases, such as digital wallets or instant payment systems, the money is transferred almost immediately.

How Modern Payment Infrastructure Improves Business Performance?

Modern payment infrastructure plays a big role in how well businesses perform. It is especially beneficial in this digital economy, where customers expect fast and convenient payment experiences. Here’s how it helps businesses grow:

1. Higher Conversion Rates

When checkout is simple and reliable, more customers complete their purchases instead of abandoning them. A strong payment infrastructure reduces friction at checkout, which directly improves conversion rates and helps businesses turn more visitors into paying customers.

2. Faster Checkout Experiences

A reliable payment processing infrastructure enables quick payments through features like saved cards, one-click checkout, and digital wallets. This reduces the time it takes for customers to pay, making the overall experience faster and more convenient.

3. Multiple Payment Methods

Today’s customers prefer different ways to pay. For instance, credit cards, debit cards, Apple Pay, Google Pay, BNPL, and even bank transfers. A strong payment infrastructure supports all of these options, giving customers flexibility and improving the chances of completing a sale.

4. Better Payment Success Rates

For businesses, maintaining a high payment success rate is essential. Modern payment infrastructure uses intelligent routing, real-time processing, and fraud prevention tools to minimize failed transactions and ensure more payments go through successfully.

5. Global Expansion Opportunities

Modern payment infrastructure makes it easier for U.S. businesses to accept international payments in multiple currencies. It handles cross-border processing, currency conversion, and compliance, allowing companies to expand globally without building complex systems from scratch.

Introducing Credee: Your Complete Payment Ecosystem

| Credee empowers businesses to create their own Revenue Builder. Through this software, businesses can create customized checkout experiences, offer flexible payment options, automate payment recovery, and collect customer feedback. For businesses searching for the best payment infrastructure for SaaS, Credee provides the flexibility and intelligence needed to optimize every transaction. Moreover, it analyzes your payment experience in real time and assigns a performance score based on how likely customers are to complete their checkout. It then delivers actionable recommendations. |

The Final Note

For businesses, choosing the right payment infrastructure is becoming increasingly important. A strong setup can improve checkout experiences and help expand into new markets. On the other hand, a weak or outdated system can lead to lost sales, frustrated customers, and operational challenges.

All in all, enterprise payment infrastructure is no longer just a technical backend function. In today’s digital-first economy, it is a direct driver of business growth.

FAQs

Q. What Is Payment Infrastructure?

Payment infrastructure is the system of technologies and banks that helps move money securely between customers and businesses during a transaction.

Q. What Is the Difference Between a Payment Gateway and a Payment Processor?

The gateway captures payment information at checkout, and the processor handles communication between banks to complete the payment.

Q. How Do Online Payments Work?

Online payments work by sending transaction details through a secure system where banks verify, approve, and transfer funds.

Q. What Are the Main Components of Payment Infrastructure?

The main components are gateways, processors, issuing and acquiring banks, card networks, and fraud prevention tools.

Q. Why Is Payment Infrastructure Important for E-Commerce Businesses?

Strong payment infrastructure reduces failed transactions and supports multiple payment methods, helping e-commerce businesses grow.